4 Non-Ferrous Metal Mining Stocks Countering Industry Headwinds

The prospects of the Zacks Mining – Non Ferrous industry look bleak as weak demand in China has been weighing on metal prices. Industry players are also grappling with inflated costs, labor shortages and supply-chain issues. However, the demand for non-ferrous metals is expected to be supported by the energy-transition trend, which will buoy the industry.

Against this backdrop, we suggest keeping a close eye on companies like Southern Copper Corporation SCCO, Ero Copper ERO, Coeur Mining CDE and Centrus Energy LEU. These companies are poised to gain from their endeavors to build reserves and control costs, while investing in technology and improving production efficiency.

About the Industry

The Zacks Mining – Non Ferrous industry comprises companies that produce non-ferrous metals, including copper, gold, silver, cobalt, molybdenum, zinc, aluminum and uranium. These metals are utilized by various industries, including aerospace, automotive, packaging, construction, machinery, electronics, transportation, jewelry, chemical and nuclear energy. Mining is a long, complex and capital-intensive process. Significant exploration and development to evaluate the size of the deposit, followed by the assessment of ways to extract and process ore efficiently, safely and responsibly, precede the actual mining operations. Miners continuously seek opportunities to grow their reserves and resources through targeted near-mine exploration and business development. They strive to upgrade and improve the quality of their existing assets internally and through acquisitions.

What’s Shaping the Future of the Mining – Non Ferrous Industry?

Volatility in Metal Prices is Concerning: Copper prices rose a meager 2% in 2023 mainly due to a slump in China demand. Contraction in the country’s construction and manufacturing sector impacted the metal’s demand. The property crisis in China has also negatively impacted prices. Despite being pitted against record-high interest rates, gold gained 13% in 2023 on safe-haven demand triggered by the banking crisis earlier in the year and the geopolitical instability. Gold has trended lower lately after the Fed pushed back strongly against expectations of a U.S. rate cut by March 2024. Gold prices have dipped 0.4% in the past month. Silver prices dipped 1.2% in 2023 mainly due to weak industrial demand. Prices have been down 2.7% in January 2024 due to the ongoing contraction in the manufacturing sector. Uranium, meanwhile, has performed well, gaining on robust demand and tight supply. The recent declaration from Kazatomprom, the world’s largest uranium mining company based in Kazakhstan, stating its intention to limit uranium production to 80% of the permitted maximum output, as specified in Kazakh subsoil usage contracts, has led to a spike in uranium prices. Overall, industry players are dealing with depleting resources, declining supply in old mines and a lack of new mines. Development projects are inherently risky and capital-intensive. While demand has been strong, there will be an eventual deficit in metal supply, leading to a situation that will bolster metal prices. This, in turn, will favor the industry in the long haul.

Labor Shortage, High Costs Remain Worrisome: The industry has been facing a shortage of skilled workforce lately, which has hiked wages. Labor-related disputes can be damaging to production and revenues. Industry players are grappling with escalating production costs, including electricity, water and materials, as well as higher freight expenses and supply-chain issues. Since the industry cannot control the prices of its products, it focuses on improving the sales volume, increasing the operating cash flow and lowering unit net cash costs. Industry participants are opting for alternate energy sources to minimize fuel-price volatility and secure supply. Miners are now committed to cost-reduction strategies and digital innovation to drive operating efficiencies.

Strong Demand to Support the Industry: The demand for non-ferrous metals will remain high in the future, given their wide use in primary sectors, including transportation, electricity, construction, telecommunication, energy and information technology. The demand for electric vehicles and renewable energy is expected to be a significant growth driver for metals like copper and nickel in the years to come. The plan to overhaul and upgrade the nation’s infrastructure, and promote green policies per the U.S. Infrastructure Investment and Jobs Act will also require a huge amount of non-ferrous metals.

Zacks Industry Rank Indicates Bleak Prospects

The group’s Zacks Industry Rank, basically the average of the Zacks Rank of all the member stocks, indicates dull prospects for the near term. The Zacks Mining – Non Ferrous industry, a 10-stock group within the broader Zacks Basic Materials Sector, currently carries a Zacks Industry Rank #186, which places it in the bottom 26% of 250 Zacks industries. Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than 2 to 1.

Before we present a few stocks that you may want to consider for your portfolio, let us look at the industry’s recent stock-market performance and its valuation picture.

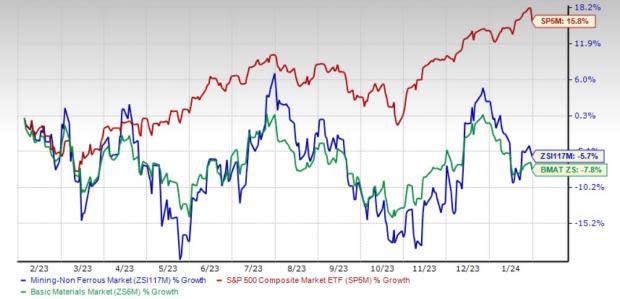

Industry Versus S&P 500 & Sector

The Zacks Mining- Non Ferrous Industry has outperformed its sector but lagged the Zacks S&P 500 composite over the past 12 months. The stocks in this industry have collectively declined 5.7% in the past year compared with the Zacks Basic Materials sector’s fall of 7.8%. The S&P 500 has grown 15.8% in the said time frame.

One-Year Price Performance

Industry’s Current Valuation

Based on the forward 12-month EV/EBITDA ratio, a commonly used multiple for valuing Mining- Non Ferrous stocks, we see that the industry is currently trading at 7.08X compared with the S&P 500’s 11.28X. The Basic Materials sector’s trailing 12-month EV/EBITDA is at 6.58X. This is shown in the charts below.

Enterprise Value/EBITDA (EV/EBITDA) Ratio (F12M)

Enterprise Value/EBITDA (EV/EBITDA) Ratio (F12M)

Over the last five years, the industry traded as high as 8.88X and as low as 3.35X, the median being 6.52X.

4 Mining – Non Ferrous Stocks to Keep an Eye on

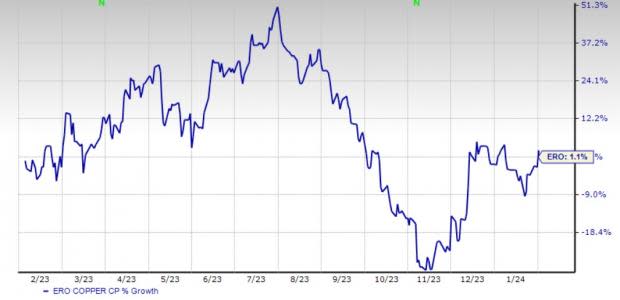

Ero Copper: The company has been progressing with its strategic initiatives, which will drive significant near-term growth. Among these, the construction of the Tucumã Project is running on schedule and is 85% completed so far. The production of copper concentrate is scheduled to commence in the second half of 2024. At the Caraíba Operations, ERO is focused on advancing its Pilar 3.0 initiative, designed to support sustained annual ore production levels of 3.0 million tons. Production from the new Matinha vein commenced at the Xavantina Operations, contributing to a quarter-over-quarter increase of more than 40% in the third quarter of 2023 to processed gold grades and gold production, as well as record-low unit operating costs. ERO is on track to double copper production to more than 100,000 tons in 2025 and expects to achieve higher sustained gold production levels of 55,000-60,000 ounces per year beginning in 2024.

The Zacks Consensus Estimate for the Vancouver, Canada-based company’s fiscal 2024 earnings indicates year-over-year growth of 102%. The estimate has moved up 7% in the past 30 days. The company engages in the exploration, development and production of mining projects in Brazil. It produces and sells copper concentrate from the Caraíba operations, located within the Curaçá Valley, northeastern Bahia state, along with gold and silver by-products. ERO currently flaunts a Zacks Rank #1 (Strong Buy).

You can see the complete list of today’s Zacks #1 Rank stocks here.

Price: ERO

Coeur Mining: The company’s fourth-quarter 2023 production reached record levels of 1.3 million ounces of silver and 19,847 ounces of gold, which marked year-over-year increases of 38% and 71%, respectively. The upbeat results were driven by the initial surge of ounces produced from the new Stage 6 leach pad and new Merrill-Crowe process plant, which began delivering silver and gold ounces late in the third quarter of 2023. Ramp-up activities at Rochester are expected to be completed in the first half of 2024. At full capacity, throughput levels are expected to average 32 million tons per year, which is 2.5 times higher than historical levels. This will make Rochester one of the world’s largest open-pit heap leach operations. Exploration success continues at Silvertip and Kensington, which bodes well for the company’s long-term growth. The highlights from surface and underground expansion drilling completed last year continue to support Silvertip’s status as one of the world’s highest-grade, undeveloped carbonate replacement deposits.

This Chicago, IL-based company explores, develops and produces gold, silver, zinc and lead properties, with five operations in the United States, Mexico and Canada. The Zacks Consensus Estimate for CDE’s fiscal 2024 earnings suggests a year-over-year improvement of 142%. The consensus estimate has moved up 60% in the past 30 days. The company currently carries a Zacks Rank #2 (Buy).

Price: CDE

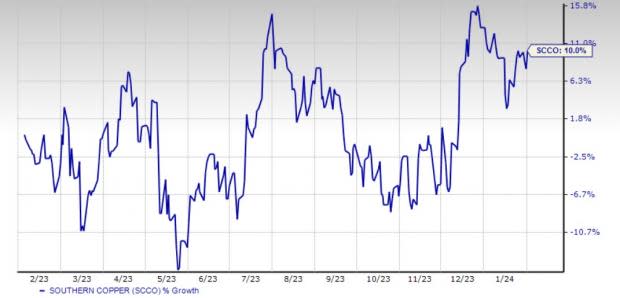

Southern Copper: The company has the largest copper reserves in the industry and operates world-class assets in investment-grade countries, such as Mexico and Peru. Its constant focus on increasing low-cost production is commendable. The company’s capital investment program for this decade exceeds $15 billion and includes investments at the Buenavista Zinc, Pilares, El Pilar and El Arco projects in Mexico, and at the Tia Maria, Los Chancas and Michiquillay projects in Peru. Backed by its project pipeline, Southern Copper has set a production target of 1.6 million tons of copper by 2032. Given its constant commitment to increasing low-cost production and growth investments, the company is well-poised to continue delivering an enhanced performance.

The Phoenix, AZ-based company has a trailing four-quarter earnings surprise of 11%, on average. The Zacks Consensus Estimate for SCCO’s fiscal 2024 earnings suggests year-over-year growth of 4%. The company, which engages in mining, exploring, smelting, and refining copper and other minerals, currently carries a Zacks Rank #3 (Hold).

Price: SCCO

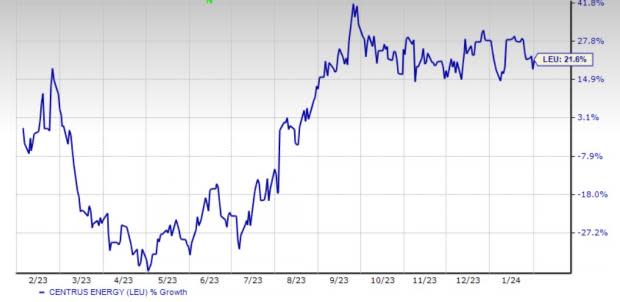

Centrus Energy: The company started the production of High-Assay Low-Enriched Uranium (“HALEU”) at its American Centrifuge Plant in Piketon, OH, in October 2023. It is the first U.S.-owned uranium enrichment plant to begin production since 1954. After making its first delivery of HALEU to the U.S. Department of Energy, completing phase One of its contract with the Department, Centrus will now move on to phase two of the contract, which required a full year of HALEU production at the rate of 900 kilograms per year at the Ohio facility. Being the only company in the United States licensed to produce HALEU, Centrus Energy has an edge over its peers. Subject to the availability of funding, Centrus Energy has the capability to expand the HALEU production at the Piketon facility and produce Low-Enriched Uranium for the existing reactors.

Headquartered in Bethesda, MD, Centrus Energy is a globally recognized supplier of Low-Enriched Uranium fuel. The Zacks Consensus Estimate for fiscal 2024 earnings has been unchanged over the past 30 days. LEU has a trailing four-quarter earnings surprise of 47.7%, on average. The company currently carries a Zacks Rank of 3.

Price: LEU

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Southern Copper Corporation (SCCO) : Free Stock Analysis Report

Coeur Mining, Inc. (CDE) : Free Stock Analysis Report

Ero Copper Corp. (ERO) : Free Stock Analysis Report

Centrus Energy Corp. (LEU) : Free Stock Analysis Report