A Look At The Truthful Worth Of NZ Windfarms Restricted (NZSE:NWF)

Right now we’ll do a easy run by means of of a valuation methodology used to estimate the attractiveness of NZ Windfarms Restricted (NZSE:NWF) as an funding alternative by taking the anticipated future money flows and discounting them to at present’s worth. We’ll use the Discounted Money Movement (DCF) mannequin on this event. Earlier than you assume you will not be capable of perceive it, simply learn on! It is truly a lot much less complicated than you’d think about.

Corporations may be valued in a whole lot of methods, so we’d level out {that a} DCF will not be good for each scenario. In case you nonetheless have some burning questions on the sort of valuation, check out the Simply Wall St analysis model.

See our latest analysis for NZ Windfarms

What’s The Estimated Valuation?

We’re going to use a two-stage DCF mannequin, which, because the title states, takes into consideration two levels of progress. The primary stage is mostly a better progress interval which ranges off heading in direction of the terminal worth, captured within the second ‘regular progress’ interval. Within the first stage we have to estimate the money flows to the enterprise over the following ten years. Seeing as no analyst estimates of free money circulate can be found to us, we’ve got extrapolate the earlier free money circulate (FCF) from the corporate’s final reported worth. We assume firms with shrinking free money circulate will gradual their fee of shrinkage, and that firms with rising free money circulate will see their progress fee gradual, over this era. We do that to mirror that progress tends to gradual extra within the early years than it does in later years.

Usually we assume {that a} greenback at present is extra helpful than a greenback sooner or later, and so the sum of those future money flows is then discounted to at present’s worth:

10-year free money circulate (FCF) forecast

|

2023 |

2024 |

2025 |

2026 |

2027 |

2028 |

2029 |

2030 |

2031 |

2032 |

|

|

Levered FCF (NZ$, Tens of millions) |

NZ$3.38m |

NZ$3.04m |

NZ$2.84m |

NZ$2.72m |

NZ$2.67m |

NZ$2.64m |

NZ$2.64m |

NZ$2.66m |

NZ$2.69m |

NZ$2.73m |

|

Development Charge Estimate Supply |

Est @ -15.54% |

Est @ -10.25% |

Est @ -6.55% |

Est @ -3.96% |

Est @ -2.14% |

Est @ -0.87% |

Est @ 0.02% |

Est @ 0.64% |

Est @ 1.07% |

Est @ 1.38% |

|

Current Worth (NZ$, Tens of millions) Discounted @ 6.9% |

NZ$3.2 |

NZ$2.7 |

NZ$2.3 |

NZ$2.1 |

NZ$1.9 |

NZ$1.8 |

NZ$1.7 |

NZ$1.6 |

NZ$1.5 |

NZ$1.4 |

(“Est” = FCF progress fee estimated by Merely Wall St)

Current Worth of 10-year Money Movement (PVCF) = NZ$20m

After calculating the current worth of future money flows within the preliminary 10-year interval, we have to calculate the Terminal Worth, which accounts for all future money flows past the primary stage. For various causes a really conservative progress fee is used that can’t exceed that of a rustic’s GDP progress. On this case we’ve got used the 5-year common of the 10-year authorities bond yield (2.1%) to estimate future progress. In the identical method as with the 10-year ‘progress’ interval, we low cost future money flows to at present’s worth, utilizing a value of fairness of 6.9%.

Terminal Worth (TV)= FCF2032 × (1 + g) ÷ (r – g) = NZ$2.7m× (1 + 2.1%) ÷ (6.9%– 2.1%) = NZ$58m

Current Worth of Terminal Worth (PVTV)= TV / (1 + r)10= NZ$58m÷ ( 1 + 6.9%)10= NZ$30m

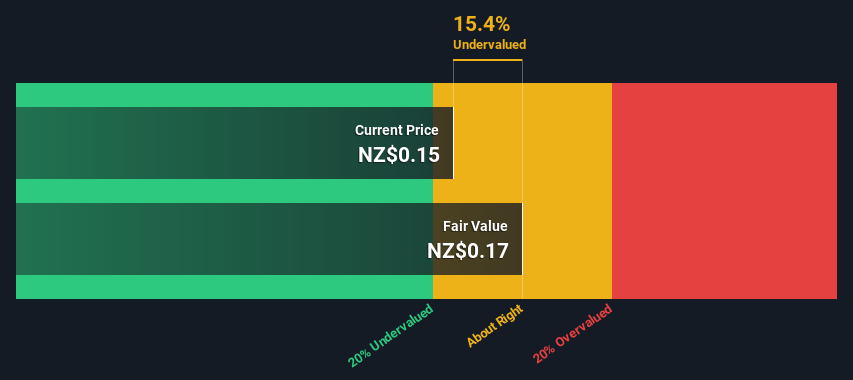

The full worth is the sum of money flows for the following ten years plus the discounted terminal worth, which ends up in the Complete Fairness Worth, which on this case is NZ$50m. The final step is to then divide the fairness worth by the variety of shares excellent. In comparison with the present share value of NZ$0.1, the corporate seems about honest worth at a 16% low cost to the place the inventory value trades presently. Valuations are imprecise devices although, slightly like a telescope – transfer a number of levels and find yourself in a special galaxy. Do preserve this in thoughts.

The Assumptions

We’d level out that an important inputs to a reduced money circulate are the low cost fee and naturally the precise money flows. In case you do not agree with these end result, have a go on the calculation your self and play with the assumptions. The DCF additionally doesn’t think about the potential cyclicality of an trade, or an organization’s future capital necessities, so it doesn’t give a full image of an organization’s potential efficiency. On condition that we’re taking a look at NZ Windfarms as potential shareholders, the price of fairness is used because the low cost fee, slightly than the price of capital (or weighted common value of capital, WACC) which accounts for debt. On this calculation we have used 6.9%, which relies on a levered beta of 0.800. Beta is a measure of a inventory’s volatility, in comparison with the market as an entire. We get our beta from the trade common beta of worldwide comparable firms, with an imposed restrict between 0.8 and a pair of.0, which is an affordable vary for a steady enterprise.

SWOT Evaluation for NZ Windfarms

Energy

Weak spot

Alternative

Risk

Transferring On:

Though the valuation of an organization is vital, it ideally will not be the only piece of study you scrutinize for an organization. The DCF mannequin will not be an ideal inventory valuation device. Relatively it must be seen as a information to “what assumptions have to be true for this inventory to be beneath/overvalued?” For example, if the terminal worth progress fee is adjusted barely, it may possibly dramatically alter the general end result. For NZ Windfarms, we have compiled three basic parts you need to additional look at:

-

Dangers: For instance, we have found 3 warning signs for NZ Windfarms that try to be conscious of earlier than investing right here.

-

Different Stable Companies: Low debt, excessive returns on fairness and good previous efficiency are basic to a robust enterprise. Why not discover our interactive list of stocks with solid business fundamentals to see if there are different firms you might not have thought-about!

-

Different Environmentally-Pleasant Corporations: Involved in regards to the atmosphere and assume customers will purchase eco-friendly merchandise increasingly? Flick through our interactive list of companies that are thinking about a greener future to find some shares you might not have considered!

PS. Merely Wall St updates its DCF calculation for each New Zealander inventory on daily basis, so if you wish to discover the intrinsic worth of every other inventory simply search here.

Have suggestions on this text? Involved in regards to the content material? Get in touch with us instantly. Alternatively, e-mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is normal in nature. We offer commentary primarily based on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles are usually not supposed to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your aims, or your monetary scenario. We intention to carry you long-term centered evaluation pushed by basic knowledge. Word that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

Be a part of A Paid Consumer Analysis Session

You’ll obtain a US$30 Amazon Present card for 1 hour of your time whereas serving to us construct higher investing instruments for the person traders like your self. Sign up here