Are Fundamentals the Driving Force of Momentum?

Mondi (LON.MNDI) stock has increased by 6.5% in the past month. We decided to examine Mondi’s (LON:MNDI) financial indicators to determine if they were a factor in the recent price movement. Stock prices are often closely linked to a company’s long-term financial performance. In particular, we chose to study Mondi’s ROE in this Article

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. ROE is short for Return on Equity. It shows how much profit each dollar generates relative to shareholder investments.

Check out our latest analysis for Mondi

How do you calculate return on equity?

The formula below can be used to calculate ROE

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders’ Equity

Based on the above formula, Mondi’s ROE is:

21% = €1.3b ÷ €6.2b (Based on the trailing twelve months to June 2022).

The company’s earnings for the past year is called its’return’. That means that for every £1 worth of shareholders’ equity, the company generated £0.21 in profit.

What does ROE have to do with earnings growth?

As we have seen, ROE is an effective indicator of a company’s future earnings. Depending on how much of these profits the company reinvests or “retains”, and how effectively it does so, we are then able to assess a company’s earnings growth potential. Companies with a higher return-on-equity and higher profit retention, assuming all else being equal, are more likely to have a higher rate of growth than those that don’t.

Comparing Mondi’s Earnings growth and 21% ROE.

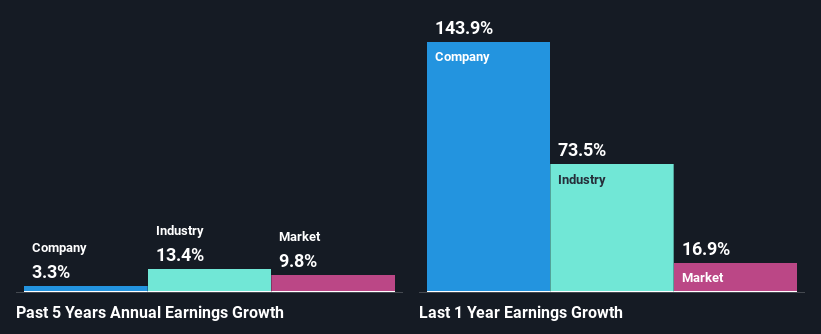

Mondi’s ROE is acceptable. The company’s ROE is also quite high compared to the industry average 17%. Mondi’s growth rate over the last five years has been a meagre 3.3%. However, this is not the norm. A company with a high rate for return should also have a high growth rate in earnings. Low growth rates and high returns could be due to poor capital allocation or earnings retention.

We next compared Mondi’s net revenue growth to industry growth and were disappointed to find that the company’s growth was lower then the industry’s average growth of 14% during the same period.

To a large extent, the earnings growth of a company is what determines whether it can be valued. Next, investors must determine if the share price already reflects the expected earnings growth. This will give investors a better idea of whether the stock is heading into brighter waters or more turbulent waters. What is MNDI worth today. The intrinsic value infographic in our free research report It helps to visualize if MNDI is currently underpriced by market.

Is Mondi Making Efficient Use Of Its Profits?

Mondi has experienced very little growth in earnings despite having a good three-year median payout ratio (or retention ratio) of 41%. This could indicate that there are other reasons for the low earnings growth. One reason could be that the business is in decline.

Mondi also has been paying dividends for at minimum ten years. This shows that the management is more concerned with maintaining the dividend payment stream than it is about business growth. The company’s future payout ratio is estimated to be 48%, according to our latest analyst data. Mondi’s future ROE, however, is expected to decrease to 11% despite the fact that there has not been much change in the company’s payout rate.

Summary

It appears that Mondi has some good aspects to its business. However, the low growth in earnings is somewhat concerning. This is especially because the company has a high return on its investment and is reinvesting large amounts of its profits. It seems like there may be other factors that are preventing growth, but they might not be in the control of the company. However, when we looked at the current analyst estimates, it was clear that the company’s earnings have increased in the past but that analysts anticipate its earnings to decrease in the future. This article will provide more information about the company’s earnings growth projections for the future. No cost report on analyst forecasts for the company to find out more.

Give feedback about this article Are you concerned about the content? Get in touch Contact us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St has a general nature. Our commentary is based only on historical data and analyst projections. This analysis does not represent a recommendation to purchase or sell any stock and it does not consider your financial goals or financial situation. Our aim is to give you long-term focused analysis that is based on fundamental data. Please note that our analysis might not include the most recent announcements from price-sensitive companies or qualitative material. Simply Wall St does not hold any position in the stocks mentioned.

Participate in a Paid User Research Session

You’ll receive a Amazon Gift Card: US$30 Give us 1 hour of your time and help us create better investing tools for individual investors like you. Sign up here